Digital channels are on track to handle the majority of banking interactions in the coming years — yet only 30% of banks successfully execute their transformation strategies. Are you prepared?

The banking industry, once a bastion of traditional practices, is now undergoing a seismic shift. Digital transformation in banking is no longer a futuristic concept; it’s a present-day imperative. From the rise of mobile banking to the integration of AI, the financial landscape is being reshaped at an unprecedented pace. But what is digital transformation in banking, and what are the implications for both institutions and customers?

Simply put, digital transformation in banking involves leveraging technology to enhance every aspect of banking operations, from customer interactions to back-office processes. It’s about more than just adding a website or a mobile app; it’s about fundamentally rethinking how banking services are delivered. The digital transformation in banking industry is about creating a seamless, personalized, and efficient experience for customers while also improving operational efficiency and driving innovation for banks.

The Breadth of Transformation: Retail, Corporate, and Investment Banking

The impact of digital transformation is felt across all segments of the banking sector. Digital transformation in retail banking has led to the proliferation of mobile banking apps, instant payment systems, and personalized financial advice powered by AI. Customers now expect 24/7 access to their accounts and seamless transactions, regardless of their location.

Recognizing that the human touch remains crucial, especially for complex financial services, retail banks are also exploring ways to blend technology with empathetic human counsel to build trust and enhance perceived brand humanity.

Digital transformation in corporate banking is streamlining processes like trade finance, cash management, and treasury operations. Automation and data analytics are enabling corporations to make faster, more informed decisions. Similarly, digital transformation in investment banking is revolutionizing deal origination, risk management, and client servicing through the use of sophisticated algorithms and platforms.

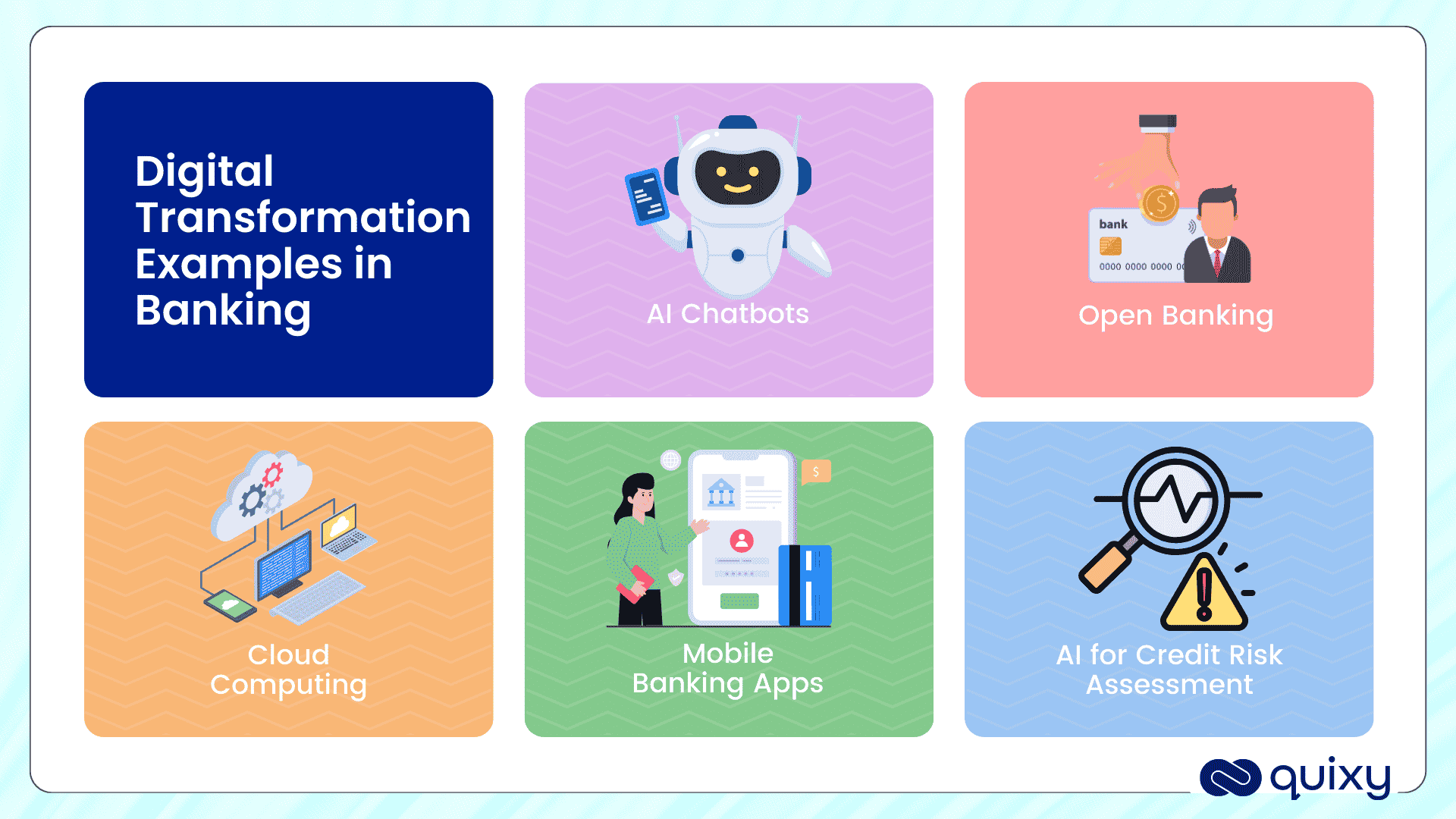

Digital Transformation Examples in Banking: From Chatbots to Blockchain

AI Chatbots

Examples of digital transformation in banking are numerous and diverse. Chatbots provide instant customer support, reducing the need for human interaction. Biometric authentication enhances security and convenience.

AI-powered chatbots offer a platter of features to automate business processes. They allow users to simply type their queries in plain text and provide instant insights using Natural Language Processing (NLP) to generate reports.

They can extract insights from PDFs, Word files, or images, allowing users to query across multiple documents to find answers and patterns. Data extraction can be automated through Intelligent Document Processing (IDP), eliminating the need for manual data entry.

A capable chatbot can pull data from various document formats and convert unstructured content into structured data, which can be displayed as reports or charts. It can even turn complex data into actionable strategies by analyzing patterns and trends.

AI chatbots can offer smarter data navigation, allowing users to use natural language queries to group, sort, and filter records. By taking user prompts and analyzing data patterns, they can also identify anomalies and irregularities in data, enabling users to take corrective actions promptly. For a bank’s customers, they can handle routine inquiries, offer 24/7 support, and assist with onboarding.

Also Explore: An Assessment to Identify Process Improvement Opportunities in Your Banks

Cloud Computing

Cloud computing allows banks to scale their operations and store data securely. Blockchain technology is being explored for its potential to streamline cross-border payments and enhance transparency.

Providing opportunities for customization, cloud platforms allow banks to easily scale their IT resources up and down based on demand. For instance, banks can utilize a pay-as-you-go model to optimize their cloud expenses and allocate resources more efficiently.

Open Banking

Digital transformation examples in banking can also be observed in the development of open banking platforms, which allow third-party developers to create innovative financial services. The deployment of AI and machine learning for fraud detection, credit scoring, and personalized financial advice are other prominent digital transformation examples.

Mobile Banking Apps

Mobile apps are a direct outcome of digital transformation, putting banking services right into the hands of customers. Through these apps, users can transfer money, pay bills, open accounts, apply for loans, and even invest—all without visiting a physical branch. Enhanced with biometric login, personalized dashboards, and AI-powered suggestions, mobile banking apps have become central to the modern banking experience.

Artificial Intelligence (AI) for Credit Risk Assessment

AI is revolutionizing credit risk assessments by enabling banks to analyze vast amounts of customer data to make more accurate lending decisions. By leveraging machine learning algorithms, banks can predict the likelihood of a customer defaulting on a loan, providing insights that improve credit scoring models. AI-based systems can process non-traditional data sources such as social media activity, transaction patterns, and behavioral data to better assess a customer’s creditworthiness, minimizing risk and making lending more inclusive.

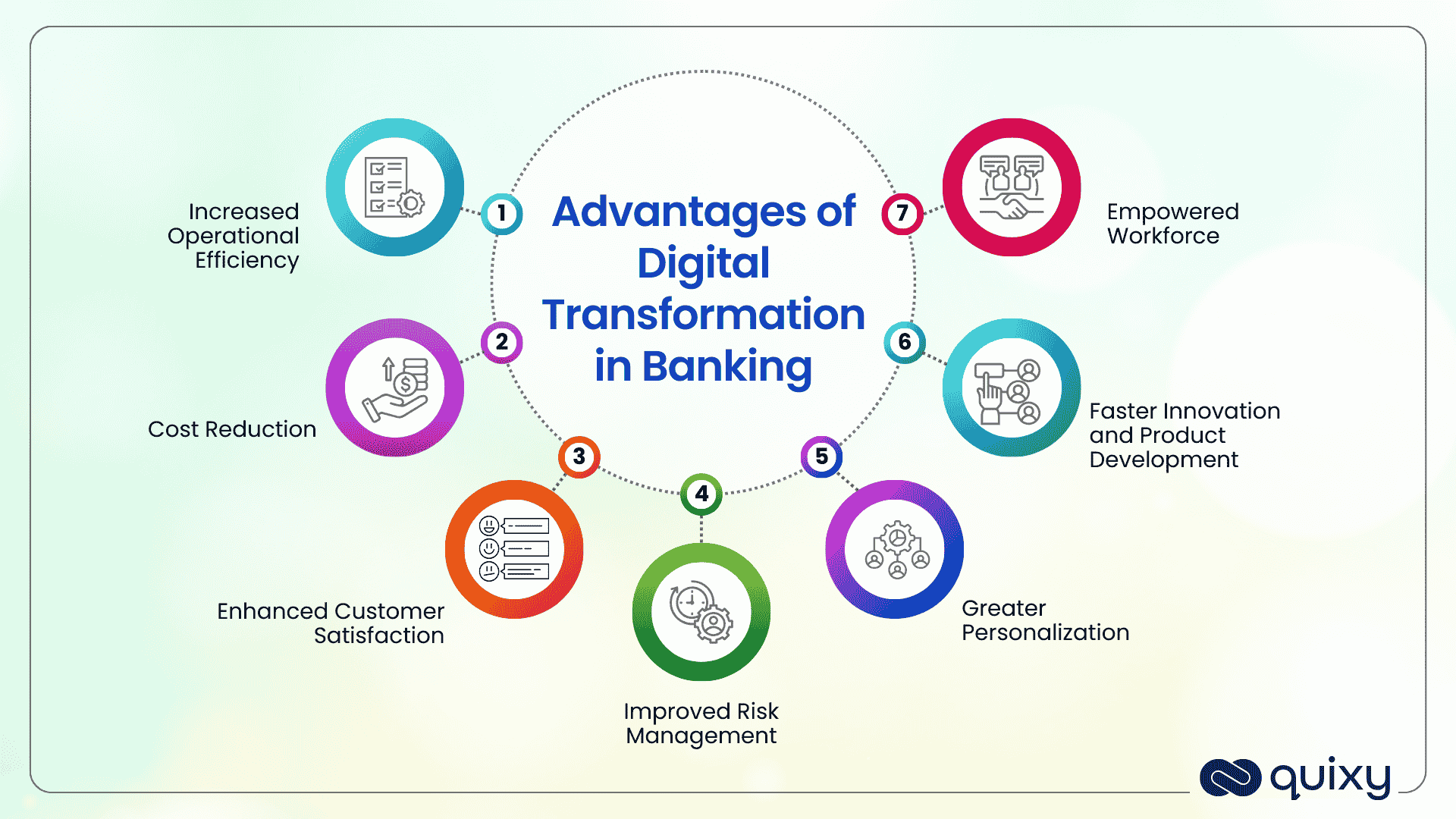

The Advantages of Digital Transformation in Banking: Efficiency, Personalization & Innovation

The benefits of digital transformation go far beyond just technology upgrades & industry trends. It empowers banks to boost efficiency, deliver hyper-personalized services, and foster innovation. By streamlining operations and leveraging data-driven insights, banks can better meet customer expectations and stay competitive in a fast-evolving financial landscape.

Increased Operational Efficiency

Automation reduces manual effort, streamlines workflows, and accelerates routine tasks across departments.

Cost Reduction

By digitizing processes and minimizing reliance on physical infrastructure and manual labor, banks can significantly lower operational expenses.

Enhanced Customer Satisfaction

Seamless digital experiences—like 24/7 access, self-service portals, and faster resolutions—improve overall customer engagement and trust.

Improved Risk Management

Advanced analytics and AI tools help banks detect fraud, assess risks more accurately, and ensure regulatory compliance.

Greater Personalization

Data-driven insights allow banks to offer tailored products, services, and communication to meet individual customer needs.

Faster Innovation and Product Development

Digital tools and platforms enable banks to quickly create and launch new offerings to adapt to changing market demands.

Empowered Workforce

Automation frees up staff to focus on strategic, high-value tasks, boosting productivity and job satisfaction.

Digital transformation drives innovation, enabling banks to develop new products and services that meet the evolving needs of their customers. This innovation is crucial for staying competitive in a rapidly changing market.

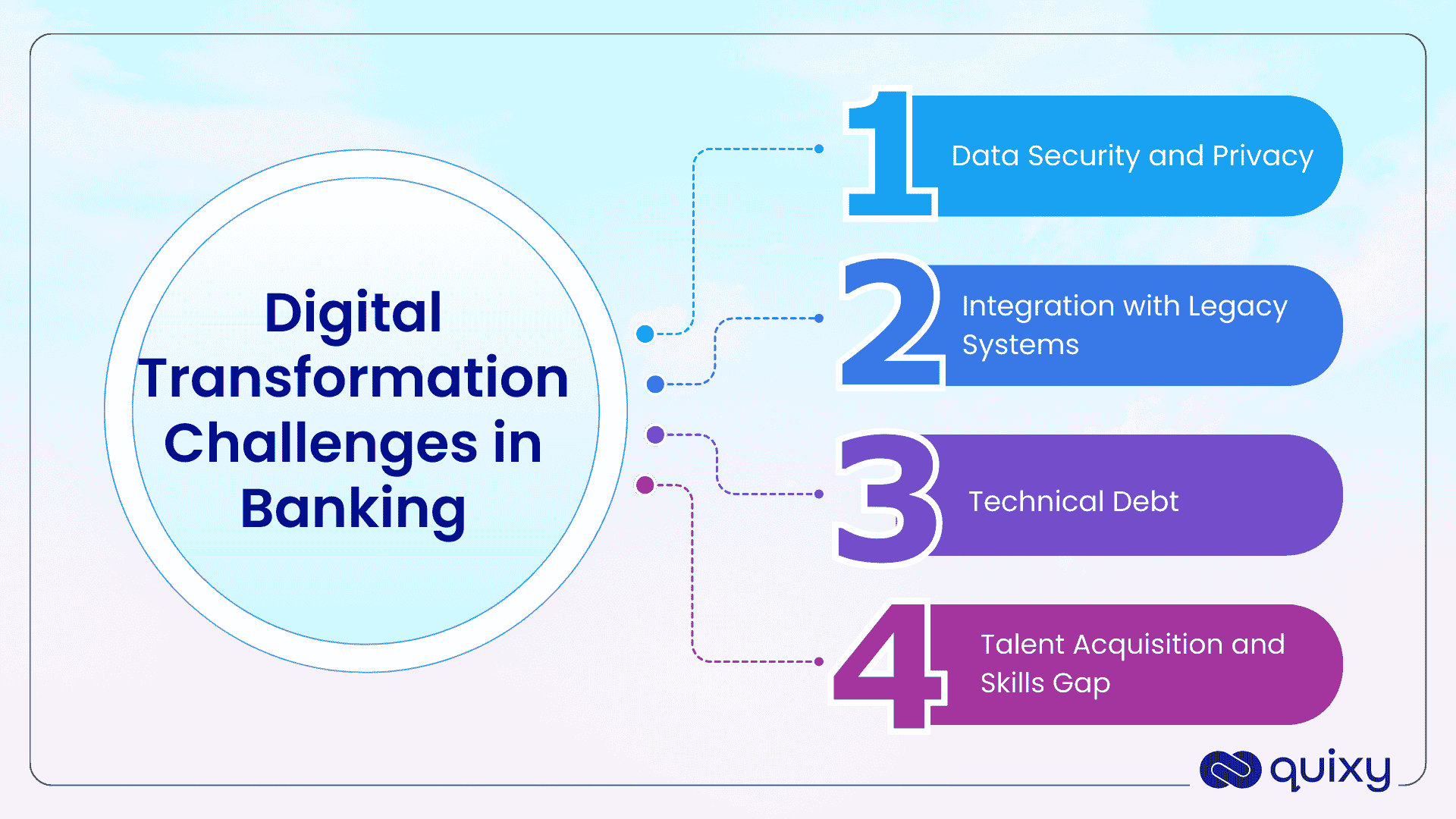

Digital Transformation Challenges in Banking

Data Security and Privacy

One of the biggest challenges in digital transformation for banks is ensuring the security of sensitive financial data. Banks must implement robust security measures to protect against cyber threats and comply with privacy regulations.

Integration with Legacy Systems

Many banks continue to operate with outdated infrastructure that is difficult to integrate with modern technologies. Overcoming this challenge requires significant investment and strategic planning to avoid disruption during the transition.

Technical Debt

Research from Boston Consulting Group, based on a study of 900 digital transformations, found that only 30% were fully successful (BCG). In banking specifically, a majority of institutions face challenges due to technical debt and struggle to quantify the impact of their digital initiatives accurately.

Also Explore: [eBook] Tech Debt in Banking: How it is holding you back

Talent Acquisition and Skills Gap

As digital transformation in banking accelerates, banks face difficulties in hiring and retaining employees with specialized skills in areas like AI, data science, and cybersecurity. To overcome this, banks must invest in continuous training and development programs to bridge the skills gap.

Overcoming Digital Transformation Challenges in Banking

Adopting Low-Code No-Code (LCNC) Platforms

One of the ways banks can overcome the challenge of integrating new technologies with legacy systems is by adopting low-code/no-code (LCNC) platforms. LCNC platforms allow for faster development and deployment of digital solutions without requiring deep technical expertise. These platforms enable banks to quickly build, customize, and integrate applications with existing infrastructure, streamlining processes and reducing the need for extensive IT resources.

Enhancing Data Security with AI

AI plays a critical role in enhancing data security in the banking sector. AI-powered solutions, such as predictive analytics and machine learning models, can identify and mitigate potential cybersecurity threats in real time. Banks can use AI to continuously monitor for suspicious activity, detect fraud, and ensure compliance with regulatory requirements.

Automating Legacy System Integration with AI and LCNC

AI and LCNC platforms can also assist in automating the integration of legacy systems with modern technologies. With AI-driven process automation and no-code development tools, banks can bridge the gap between old and new systems, reducing the complexity of data migration and enhancing operational efficiency. These solutions provide seamless integration, allowing banks to maintain their legacy systems while gradually adopting more advanced, future-proof technologies. This minimizes the disruption that often accompanies digital transformation, ensuring smoother transitions and better overall performance.

Digital Transformation Trends in Banking: AI, Cloud, and Beyond

Several key digital transformation trends are shaping the banking industry’s future. Artificial intelligence (AI) is transforming customer service, risk management, and fraud detection. Cloud computing is enabling banks to scale their operations and reduce costs. Open banking is fostering innovation and competition.

The rise of fintech companies is also driving digital transformation. These agile startups are challenging traditional banks by offering innovative financial services. The adoption of blockchain technology for secure and transparent transactions is another significant trend.

Neobanks and fintechs are also setting a faster pace of innovation, typically releasing new features far more quickly than traditional banks, whose release cycles are often slowed by legacy infrastructure and compliance review.

Digital Transformation in Banking and Financial Services: A Broader Perspective

The impact of digital transformation extends beyond traditional banking to the broader financial services industry. Digital transformation in banking and financial services is reshaping insurance, asset management, and other related sectors. The integration of technology is creating a more interconnected and efficient financial ecosystem.

Also Explore: [eBook] A Guide to Measure Quixy’s ROI in Banking

The Future of Digital Transformation in Banking: Personalized, Secure, and Seamless

The future of digital transformation in banking is bright. As technology continues to evolve, banks will have even more opportunities to enhance their services and improve the customer experience. The focus will be on creating personalized, secure, and seamless financial solutions.

Digital Transformation in Banking Examples

A digital transformation in banking case study often highlights the success of institutions fully embracing technological change. Some banks have successfully implemented AI-powered chatbots to handle customer queries, dramatically reducing wait times and improving satisfaction. Others have leveraged data analytics to personalize financial advice, increasing customer engagement and loyalty.

Singapore-based DBS bank realized it needed to cater to next-gen tech-savvy users by becoming a digitally driven bank. The bank developed its new operating model around 33 platforms aligned to business segments and products. DBS has publicly discussed significantly compressing its AI and technology deployment timelines as part of its platform-based operating model, restructured around business-aligned technology teams.

Also Read: How Quixy Can Help You with Digital Transformation

Quixy for Banking Digital Transformation: Effortless Management & AI-Powered Oversight

Quixy’s no-code low-code digital transformation platform empowers banks with effortless management through centralized control and intelligent automation. With a unified dashboard, administrators can monitor all banking applications, workflows, and user activities from a single interface. Its drag-and-drop governance allows for easy adjustments to permissions, roles, and approvals—no coding required. The platform’s cloud-native, auto-scaling infrastructure ensures seamless performance even during peak loads like month-end reporting.

Quixy offers granular admin control through role-based access (RBAC), enabling precise permission settings tailored to specific roles, such as tellers or loan officers. Comprehensive audit trails help maintain compliance with regulations like SOX and GDPR, while one-click rollbacks make it simple to revert changes instantly in case of errors.

Quixy’s AI Agent Caddie further enhances operations by delivering smart reports and anomaly detection. Using natural language queries, users can generate real-time insights—for example, liquidity ratios or high-risk loan summaries—and automate scheduled PDF or Excel exports for stakeholders. The platform’s machine learning capabilities also flag unusual patterns, such as fraudulent transactions or sudden spikes in deposits, and even recommend corrective actions like freezing suspicious accounts.

Case Studies: Quixy’s Impact on Banking & Insurance

1. SUCO Bank: Streamlining Non-Core Banking Processes

SUCO Bank, a fast-growing cooperative bank in Karnataka, India, faced inefficiencies in manual, paper-based processes like HR appraisals, lead management, and procurement. These workflows were slow, error-prone, and lacked transparency.

Challenges:

- Manual Processes: Email/paper-based systems caused delays (e.g., appraisal turnaround took weeks).

- Disconnected Tools: Needed a unified platform for non-core processes alongside core banking systems.

- Scalability Issues: Expanding branch network demanded agile solutions.

Quixy’s Solution:

- No-Code Automation: Built custom apps for HRMS, IT incident management, and inventory tracking without coding.

- Single Source of Truth: Consolidated data on one platform, eliminating redundancy.

- Agile Deployment: Implemented via citizen development, with process owners empowered to modify apps.

Results:

- 30% faster process turnaround (e.g., appraisal management).

- Reduced IT overhead by replacing multiple COTS applications with one platform.

- Enhanced transparency with real-time tracking and role-based access.

Read case study: Processes Turn-Around Time reduced by 30% for SUCO Bank

2. SAICO Insurance: Digitizing Complex IT Workflows

SAICO, a leading Saudi Arabian insurer, relied on Excel and emails for IT workflows, risking data manipulation and inefficiencies.

Challenges:

- Fragile Systems: Manual Excel-based processes lacked security and audit trails.

- Multi-Department Coordination: Approvals and collaborations were slow and opaque.

- Dynamic Requirements: Needed flexibility to adapt forms and workflows.

Quixy’s Solution:

- Low-Code Workflow Automation: Digitized IT workflows with drag-and-drop interfaces.

- Secure Access Controls: Prevented unauthorized data changes with role-based permissions.

- Real-Time Tracking: Dashboards provided visibility into SLA metrics and bottlenecks.

Results:

- 50% boost in operational efficiency by reducing manual effort.

- Enhanced Compliance: Audit trails and KPI tracking improved regulatory adherence.

- Faster Decision-Making: Real-time insights accelerated approvals.

Read case study: Quixy Drives Process Transformation: SAICO Achieves 50% Efficiency Boost

Conclusion: Embracing Digital Transformation in Banking Industry

Digital transformation in the banking industry is an unstoppable force. Banks that embrace change and invest in technology will be well-positioned to thrive in the digital age. Banks can create a sustainable and prosperous future by focusing on customer needs, leveraging innovative technologies, and addressing the challenges of transformation.

Digital transformation in banking is not a singular event but an ongoing journey of continuous evolution and adaptation. To thrive in this new era, banks must wholeheartedly embrace technological innovation and cultivate a culture of agility and customer-centricity.

The future of the banking industry will be fundamentally defined by digital capabilities, with a relentless focus on enhancing customer experience and delivering personalized value. Banks that proactively navigate this transformative landscape, prioritizing customer needs and fostering a spirit of continuous innovation, will be best positioned to survive and flourish in the digital-first world of finance.

Frequently Asked Questions(FAQs)

Q. What are the biggest challenges in banking DT?

The biggest challenges in banking digital transformation include: legacy system integration, cybersecurity risks, cultural resistance to change, and talent gaps in AI and cloud expertise.

Q. How does no-code technology benefit banks?

No-code platforms like Quixy allow banks to:

Automate processes (e.g., KYC, loan applications) without coding.

Reduce costs by minimizing IT dependency.

Scale quickly with customizable dashboards and workflows

Q. What’s the role of cloud computing in banking digital transformation?

Cloud computing enables scalability, cost efficiency, and agility. Banks can respond to changing customer demands quickly, deploy updates faster, and manage data securely. Cloud-native platforms also support real-time collaboration, disaster recovery, and faster innovation cycles.

Q. How can banks start their digital transformation journey?

Banks can begin with low-code/no-code platforms like Quixy to digitize and automate non-core processes (e.g., HR, procurement) without heavy IT investment. Empowering internal teams through citizen development allows for quick wins, iterative improvement, and reduced dependence on legacy tech stacks.

Q. What is digital transformation in banking?

Digital transformation in banking refers to the integration of digital technologies into all areas of a bank’s operations, fundamentally changing how banking services are delivered and experienced. It’s not just about launching a mobile app or online portal—it’s about reimagining processes, customer engagement, and internal workflows using technologies like AI, cloud computing, data analytics, and automation.

Related Post

Please login to comment

0 Comments

Oldest

Recent Posts

![]()

![]()

- Download the App